Strategy

Repricing Flow Strategy

Repricing Flow is a long-biased systematic L/S equity strategy designed to outperform SPY in unhedged GBP terms by buying liquid US/UK/EU equities undergoing slow institutional repricing, while using short index exposure and downside overlays to control market drawdown rather than neutralise beta.

It buys liquid stocks where fundamental improvement is confirmed by price action, but where large investors typically adjust exposure gradually because of liquidity, benchmark, mandate, and career-risk constraints.

The value proposition versus simply buying SPY is upgraded equity participation: retain exposure to the same equity-risk engine, but replace passive index ownership with a diversified, capped stock-selection book, explicit cost/liquidity discipline, and downside protection.

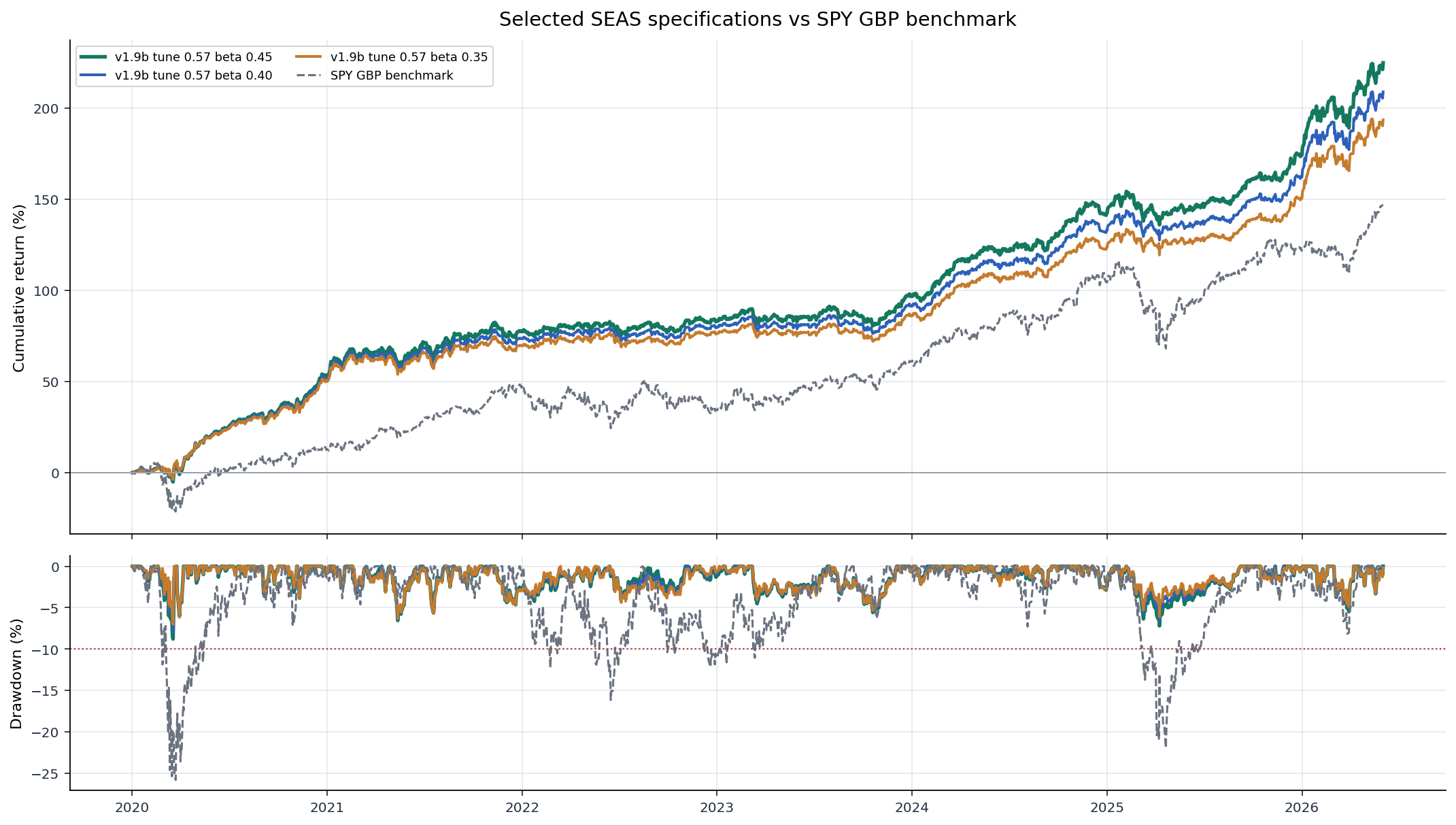

In the current Best Sharpe backtest, 2020-01-02 to 2026-06-02, the strategy returns 19.4% annualised versus 14.6% for SPY GBP, with Sharpe 2.06 versus 0.76 and max drawdown -8.8% versus -25.8%, delivering roughly +4.8% annualised excess return with materially lower realised downside.

Implementation spectrum

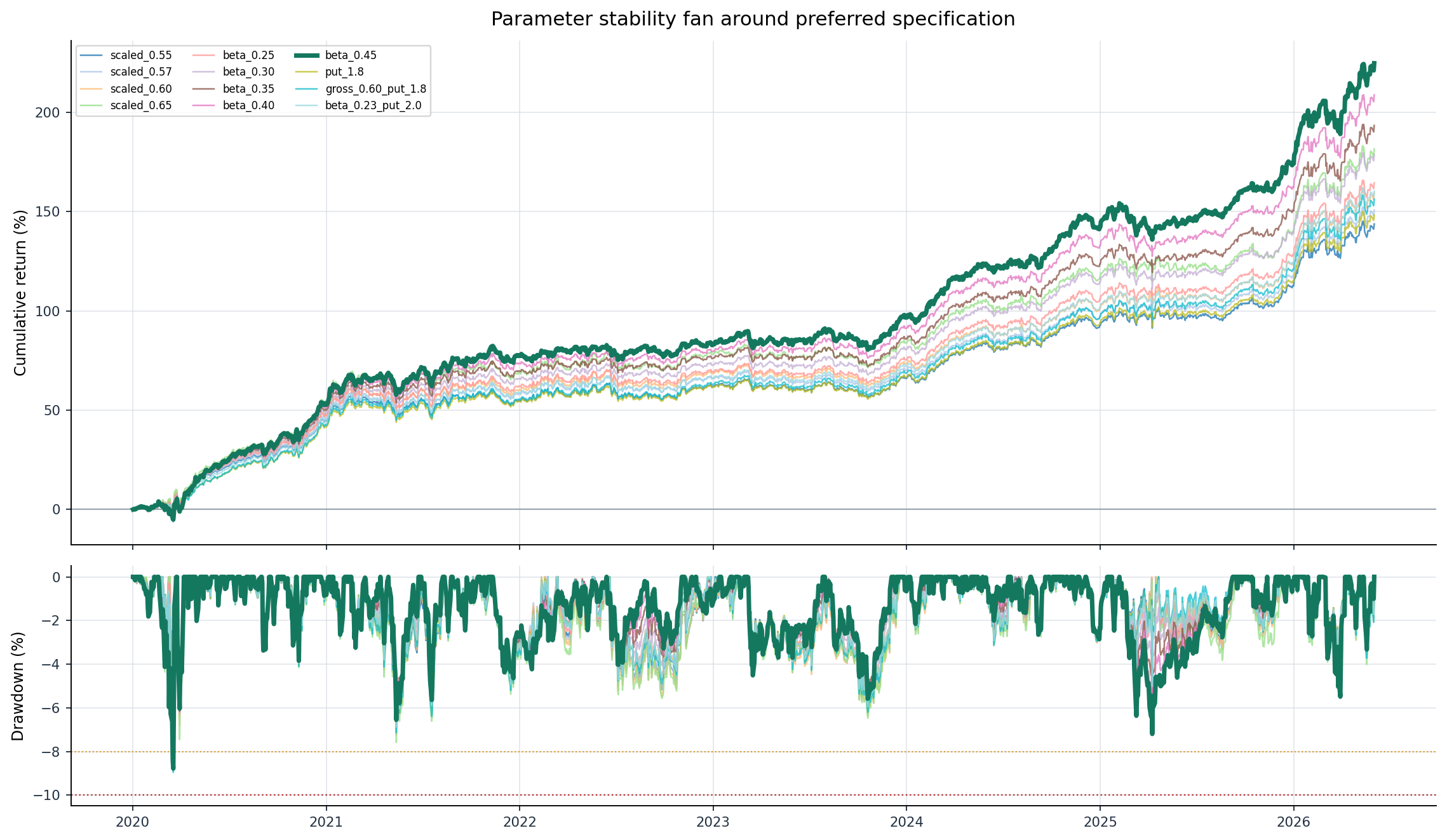

Best Sharpe, risk-tight, and conservative variants

| Role | Annualised return | Volatility | Sharpe | Max drawdown | Latest beta | Turnover | Notes |

|---|---|---|---|---|---|---|---|

| Best Sharpe specification | 19.4% | 9.4% | 2.06 | -8.8% | 0.48 | 32.0% | Lead research book. Uses more drawdown budget, but remains below the informal -10% danger line. |

| Risk-tight boundary | 18.5% | 9.4% | 1.98 | -7.9% | 0.43 | 32.0% | Tight implementation if the drawdown limit is treated as -8% rather than -10%. |

| Conservative fallback | 17.6% | 9.4% | 1.88 | -7.0% | 0.38 | 32.0% | Lower-beta version for capital-ramp or conservative implementation framing. |

Historical research output only. Figures are not live performance, target returns, investment advice, an offer, solicitation, or a recommendation.

Against SPY in unhedged GBP terms over 2020-01-02 to 2026-06-02:

| Variant | Ann. return | SPY ann. return | Annualised outperformance | Total return | SPY total return | Total outperformance |

|---|---|---|---|---|---|---|

beta045 Best Sharpe |

19.4% | 14.6% | +4.8% p.a. | 224.4% | 146.8% | +77.6 pp |

beta040 risk-tight |

18.5% | 14.6% | +3.9% p.a. | 208.5% | 146.8% | +61.6 pp |

beta035 conservative |

17.6% | 14.6% | +3.0% p.a. | 193.1% | 146.8% | +46.3 pp |

Report figures

Implementation diagnostics

Professional review